STOLEN IDENTITY, CREDIT FIGHT – Credit Bureau Violations, Fraudulent Accounts, And California Consumer Rights

Identity theft can leave fraudulent accounts, hard inquiries, collection activity, and credit damage behind

R23 Law's California Consumer Protection Attorneys represent Californians facing credit bureau violations, failed fraud disputes, and FCRA claims.

Identity Theft Can Leave Long Credit Damage

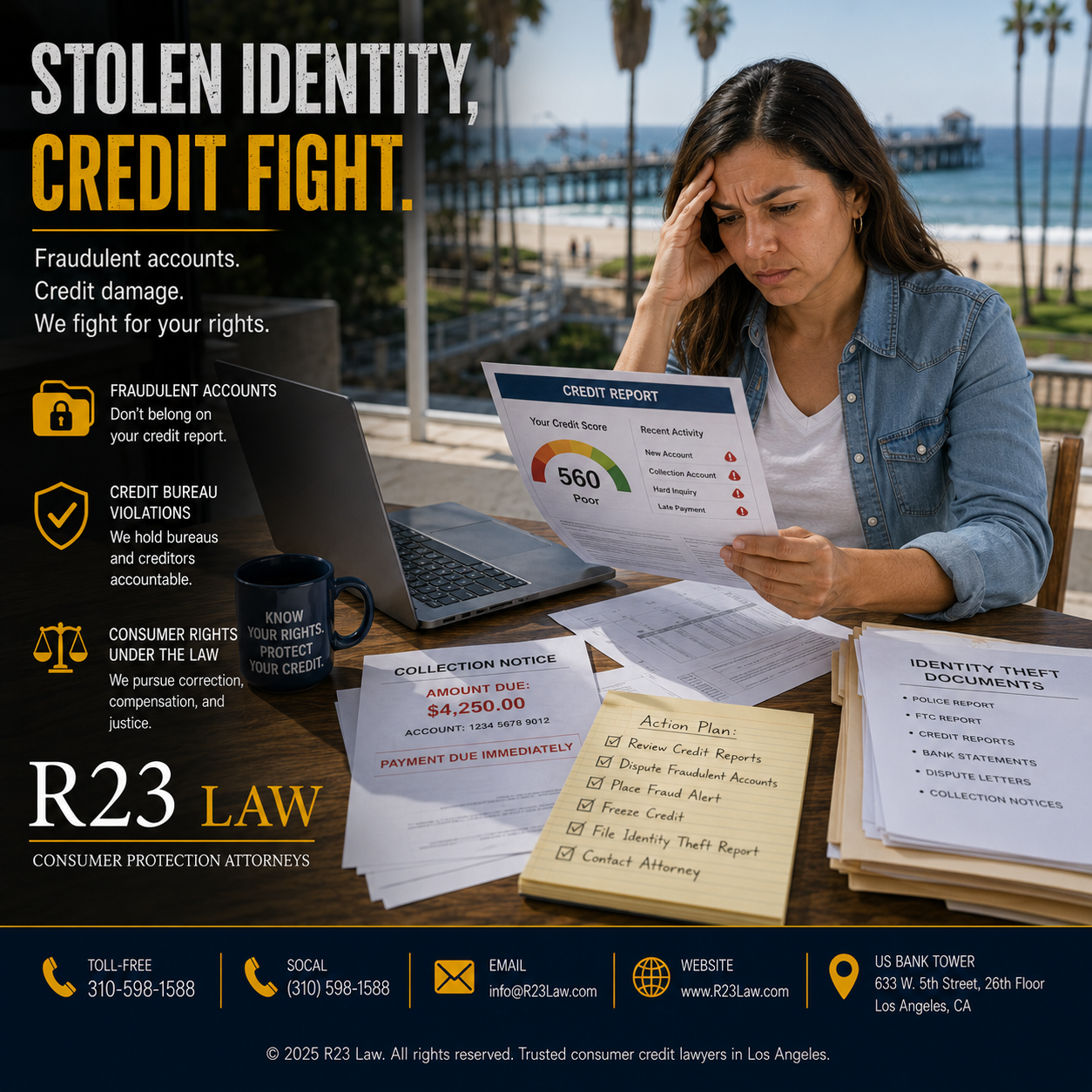

Identity theft does not end when the fraudster opens the account. The aftermath often appears on credit reports through fraudulent accounts, unauthorized hard inquiries, false balances, collection tradelines, late payments, and debt that never belonged to the consumer.

The attached source explains that fraudulent accounts can affect mortgages, car loans, credit cards, job opportunities requiring credit checks, and interest rates. It also warns that some victims mistakenly accept years of credit damage when legal rights may provide a path toward correction and recovery.

R23 Law's California Consumer Protection Attorneys represent identity theft victims dealing with Experian, Equifax, TransUnion, creditors, debt collectors, furnishers, and companies that refuse to correct fraud-related credit reporting.

Fraudulent Accounts Often Follow Patterns

Identity theft may show up as one account, but it often appears in clusters. The attached source explains that fraudulent accounts may appear close together when someone has gained access to personal information and used it to open multiple accounts in a short period. Unauthorized hard inquiries may also appear before fraudulent accounts are opened.

Consumers should review all three credit reports for:

Credit cards they never opened

Loans they never requested

Hard inquiries from unfamiliar companies

Collection accounts tied to unknown debts

Addresses they never used

Accounts opened around the same time

False late payments

Creditors they never contacted

Fraudulent accounts reported as accurate after a dispute

Checking credit reports through consumer-authorized channels does not damage credit scores. The CFPB explains that disputing credit report errors requires the credit reporting company to investigate, forward relevant information to the furnisher, and report the results back to the consumer.

Soft Inquiries, Hard Inquiries, And Fraud Clues

The attached source distinguishes between soft inquiries and hard inquiries. Soft inquiries from checking your own credit do not lower your score, while hard inquiries can occur when someone applies for credit and may affect the score.

That distinction matters for identity theft victims. Regularly reviewing credit reports can reveal suspicious applications without creating additional credit damage. The inquiry section may show the first signs that a fraudster has started applying for credit in the consumer’s name.

R23 Law's Expert Legal Services For Identity Theft Victims Throughout California

R23 Law's California Consumer Protection Attorneys evaluate identity theft credit claims involving fraudulent accounts, unauthorized inquiries, failed credit bureau investigations, debt collector misconduct, creditor reporting errors, and continued reporting after notice of fraud.

Our legal services may include reviewing credit reports, organizing fraud documentation, preparing dispute strategies, evaluating FCRA violations, pursuing credit correction, and seeking compensation where credit reporting violations caused financial or emotional harm.

Learn more about the firm through About R23 Law, meet the attorneys through Our Team, or begin through Contact Us.

Strong Documentation Can Change The Dispute

The attached source explains that generic disputes often fail because they do not provide enough detail. A stronger dispute should explain how the fraud was discovered, identify the fraudulent accounts, describe the financial impact, and include supporting evidence.

Useful documents may include:

FTC identity theft report

Police report

Credit reports with fraudulent items identified

Account statements

Denial letters

Debt collection notices

Proof of residence or employment when the account was opened

Fraud affidavits

Certified mail receipts

Written responses from credit bureaus or furnishers

IdentityTheft.gov provides sample letters for requesting that credit bureaus block fraudulent information connected to identity theft, including language referencing FCRA Section 605B.

Credit Freezes And Fraud Alerts Provide Ongoing Protection

Disputing existing fraudulent accounts addresses past harm. Preventing new accounts requires additional safeguards.

The attached source describes credit freezes as a strong defense because they limit the ability of lenders to process new applications in the consumer’s name without verification. The FTC explains that credit freezes and fraud alerts are free tools that can reduce the risk of further identity theft misuse.

The CFPB also explains that a fraud alert tells creditors to take steps to verify identity before opening new credit, issuing an additional card, or increasing a credit limit.

The 30-Day Investigation Requirement Matters

The attached source emphasizes that credit bureaus and furnishers have legal obligations after receiving disputes, including a 30-day investigation requirement. Under the FCRA, credit reporting agencies must provide notice of a dispute to the furnisher within five business days after receiving the dispute.

If a credit bureau or furnisher verifies an obviously fraudulent account without a reasonable investigation, refuses to remove fraud-related reporting, or ignores strong documentation, legal claims may be available.

When Credit Bureaus Refuse To Remove Fraudulent Accounts

Not every credit bureau or creditor responds properly. The attached source notes that some companies refuse to remove obviously fraudulent accounts, fail to investigate within the required timeframe, or conduct superficial reviews that miss clear signs of fraud.

Legal action may be necessary when dispute letters do not correct the record. Consumer protection lawsuits can pursue removal of fraudulent accounts, compensation for credit damage, emotional distress, actual financial losses, and attorney’s fees where the law allows.

R23 Law's California Consumer Protection Attorneys Pursue Credit Bureau Accountability

Identity theft victims should not be forced to carry false debts for years. Credit bureaus, furnishers, creditors, banks, lenders, and debt collectors must take fraud disputes seriously.

R23 Law's California Consumer Protection Attorneys pursue claims when companies ignore identity theft reports, fail to investigate, continue reporting fraudulent accounts, or leave consumers with credit damage caused by someone else’s fraud.

Reclaim Your Credit After Identity Theft

Fraudulent accounts can block loans, raise rates, interfere with housing, and create stress long after the theft occurs. Strong documentation, credit freezes, fraud alerts, targeted disputes, and legal review can give consumers a path toward correction and accountability.

R23 Law stands with California consumers facing identity theft, credit bureau violations, FCRA claims, fraudulent accounts, unauthorized inquiries, and debt collection tied to fraud.

Contact R23 Law Today

Identity theft can leave false accounts and credit damage that credit bureaus refuse to correct. If fraudulent accounts, unauthorized inquiries, or identity theft-related debts remain on your credit reports after a dispute, R23 Law's California Consumer Protection Attorneys can review your rights and legal options.

Contact R23 Law Today Toll-Free — 310-598-1588 SoCal — (310) 598-1588 Email — info@R23Law.com Website — www.R23Law.com US Bank Tower, 633 W. 5th Street, 26th Floor, Los Angeles, CA

© 2025 R23 Law. All rights reserved. Trusted consumer credit lawyers in Los Angeles.