COLLECTOR CALLS, LEGAL WALLS – California Consumer Rights Against Abusive Debt Collection And FDCPA Violations

Debt collectors cannot harass, threaten, deceive, or pressure consumers through illegal tactics

R23 Law's California Consumer Protection Attorneys represent Californians facing abusive debt collection, FDCPA violations, and unfair credit reporting.

Debt Collectors Cannot Cross The Line

Debt collection can be stressful enough without harassment, threats, or deception. The Fair Debt Collection Practices Act, known as the FDCPA, is a federal law that limits what third-party debt collectors can say and do when collecting certain consumer debts. It prohibits abusive, unfair, and deceptive practices.

R23 Law's California Consumer Protection Attorneys represent consumers who are being pressured by debt collectors through unlawful calls, false threats, misleading letters, inflated balances, collection of disputed debts, and credit reporting abuse.

Common Debt Collection Violations

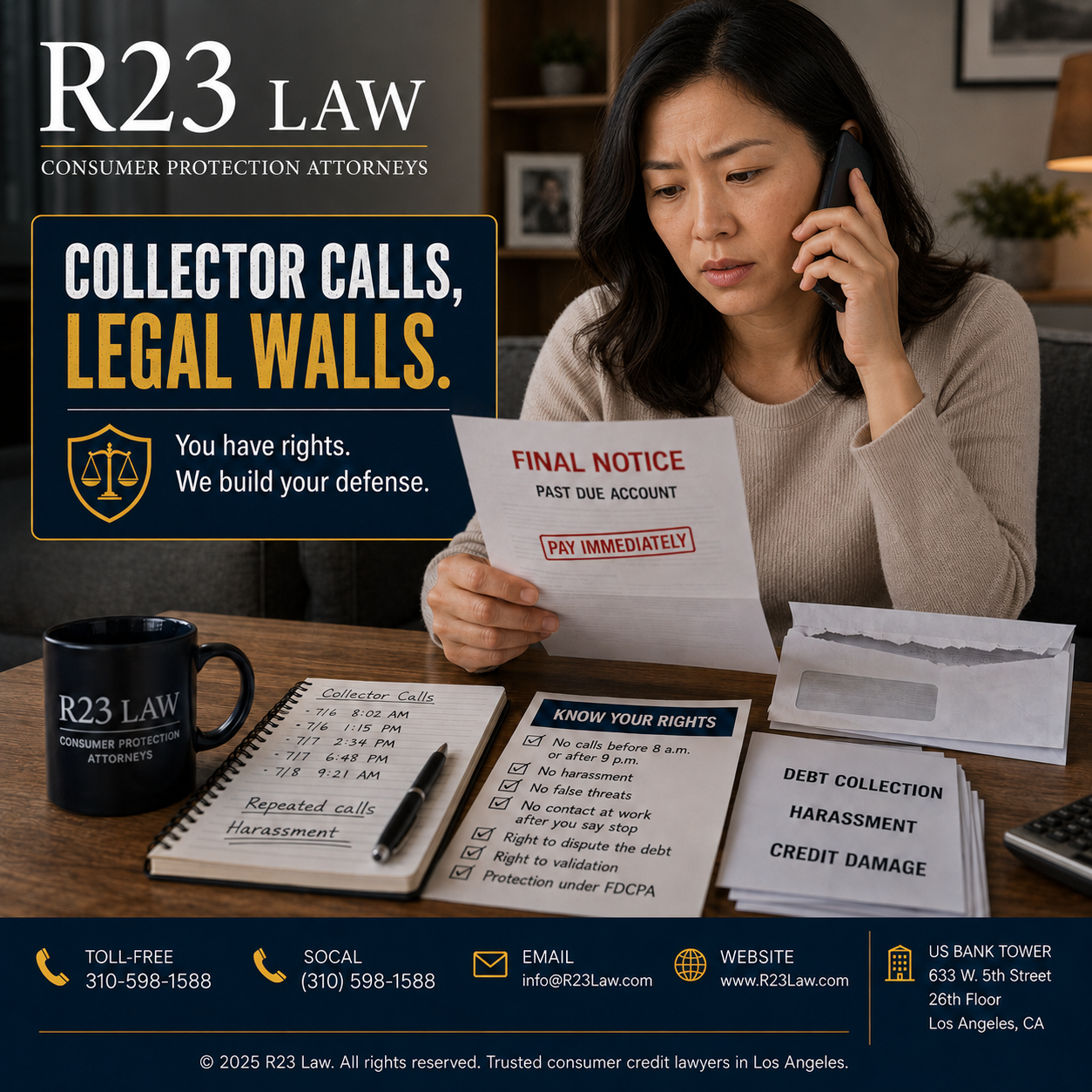

Debt collectors do not get unlimited access to your phone, workplace, family, or peace of mind. The attached source highlights several FDCPA restrictions, including limits on contact hours, repeated calls, workplace communications, attorney representation, validation disputes, and abusive collection tactics.

Common violations may include:

Calling before 8 a.m. or after 9 p.m.

Calling repeatedly to annoy, abuse, or harass

Calling your workplace after being told that work calls are not allowed

Contacting you directly after knowing you have an attorney for the debt

Continuing collection during the required validation period after a timely validation request

Using profane or abusive language

Threatening arrest

Threatening legal action that is not actually intended

Lying about the amount owed

Publishing or exposing debt information improperly

Using postcards or public-facing communications about a debt

The CFPB confirms that debt collectors generally may not contact consumers before 8 a.m. or after 9 p.m., and must follow certain consumer instructions about inconvenient times or places.

R23 Law's Expert Legal Services For California Debt Collection Victims

R23 Law's California Consumer Protection Attorneys review debt collection calls, letters, voicemails, credit reporting entries, lawsuits, and payment demands to determine whether a collector violated federal or California law.

Our legal services may include evaluating FDCPA violations, reviewing collection letters, analyzing call patterns, preserving evidence, disputing false debts, addressing credit report damage, and pursuing compensation where collectors violate consumer protection laws.

Learn more about the firm through About R23 Law, meet the attorneys through Our Team, or start through Contact Us.

Keep Records Of Every Collection Contact

Evidence matters. If a debt collector is contacting you, keep a written timeline of every call, letter, voicemail, text, email, and credit reporting event. The attached source recommends documenting calls, including the time of the call and the names of people contacting you about the debt.

Consumers should save:

Collection letters

Call logs

Voicemails

Text messages

Emails

Payment demands

Credit report entries

Dispute letters

Certified mail receipts

Notes from every conversation

These records may support claims for harassment, deception, improper contact, failure to validate, or unlawful credit reporting.

Debt Validation And Disputed Debts

When a consumer disputes a debt or requests validation during the applicable period, a debt collector must follow legal procedures before continuing collection. A collector that ignores a proper dispute, refuses to provide basic debt information, or continues pressuring payment on a questionable debt may be violating the law.

This is especially important when the debt is unfamiliar, inflated, outdated, already paid, discharged in bankruptcy, tied to identity theft, or reported inaccurately on a credit report.

R23 Law's California Consumer Protection Attorneys evaluate whether a collector had the legal right to collect and whether its communications complied with the FDCPA, the Fair Credit Reporting Act, and California consumer protection laws.

Legal Claims Against Abusive Debt Collectors

Consumers may have the right to sue debt collectors who violate the FDCPA. The attached source notes that consumers generally must file within one year from the date of the violation. The FTC likewise explains that consumers may sue a collector in state or federal court within one year from the date the law was violated.

Available recovery may include actual damages, statutory damages, attorney’s fees, and court costs, depending on the facts and claims. The attached source also notes that a court may award up to $1,000 even without proven actual damages.

R23 Law's California Consumer Protection Attorneys Pursue Collector Accountability

Collectors should not be allowed to intimidate consumers into paying debts that are false, inflated, disputed, or legally questionable. R23 Law's California Consumer Protection Attorneys pursue accountability when collection companies use unlawful pressure tactics or damage a consumer’s credit through false reporting.

Debt collection abuse can affect credit, employment, housing, health, privacy, and financial stability. Consumers have rights, and collectors must follow the law.

Contact R23 Law Today

Abusive debt collection can quickly become a credit, privacy, and financial crisis. If a debt collector is calling repeatedly, threatening legal action, contacting your workplace, misrepresenting a debt, or reporting false information, R23 Law's California Consumer Protection Attorneys can review your rights and legal options. Toll-Free — 310-598-1588