CREDIT ERRORS, REAL CONSEQUENCES – California Consumer Rights After Credit Report Errors And Failed Disputes

Credit report errors can damage credit scores, block loans, raise insurance costs, and interfere with housing or employment

R23 Law's California Consumer Protection Attorneys represent Californians facing inaccurate credit reporting, failed disputes, identity theft accounts, and FCRA violations.

Credit Report Errors Can Damage Your Financial Future

A credit report error can do more than lower a score. It can affect loan approvals, credit card applications, apartment rentals, insurance premiums, employment opportunities, and your overall financial reputation.

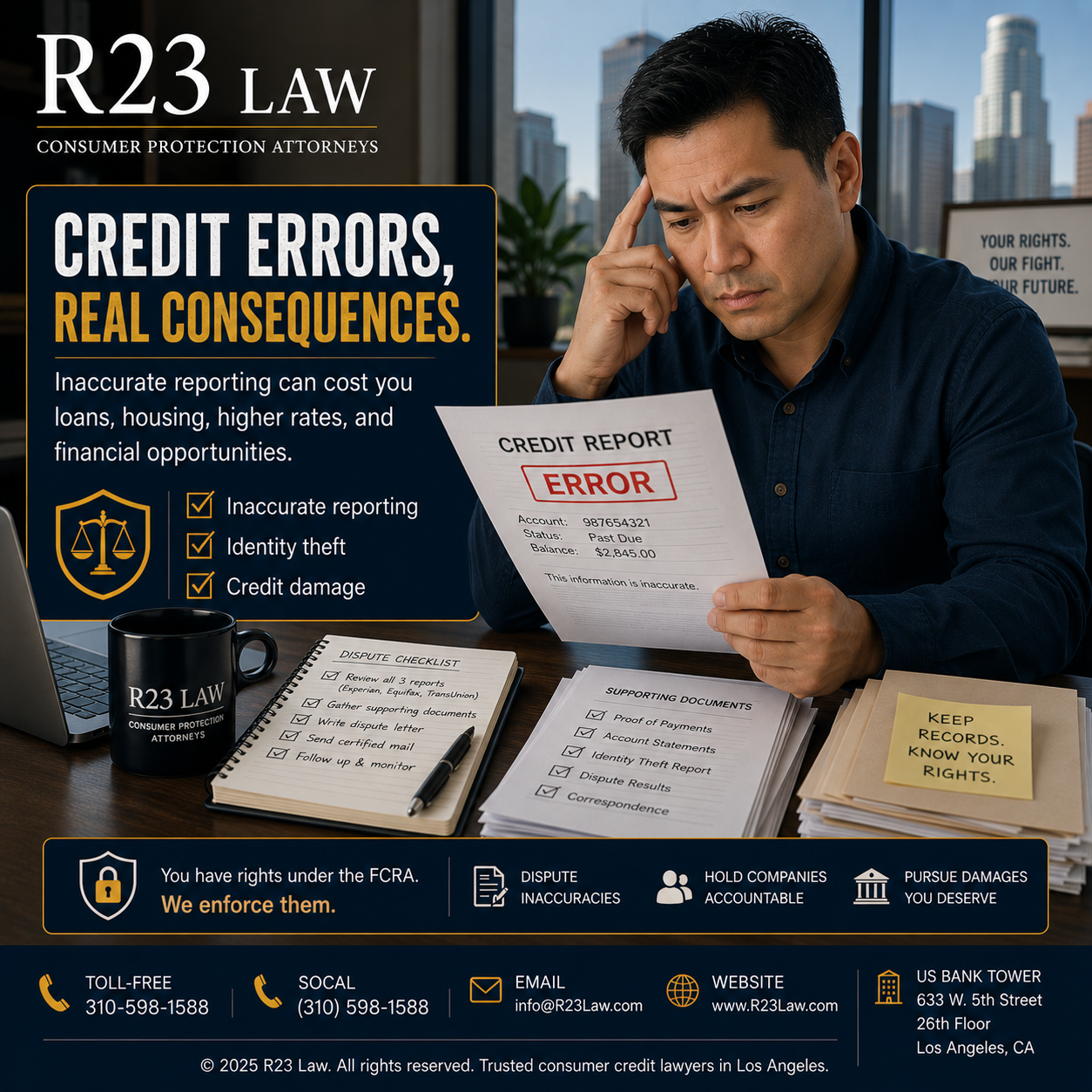

The attached source explains that consumers should review credit reports from Experian, Equifax, and TransUnion because information may vary across the three credit reporting agencies. It also identifies common errors such as incorrect balances, duplicate accounts, accounts that do not belong to the consumer, inaccurate payment history, outdated negative information, and incorrect personal details.

R23 Law's California Consumer Protection Attorneys represent consumers harmed by inaccurate credit reporting, identity theft accounts, ignored disputes, and credit bureau investigations that fall short of the law.

Common Credit Report Errors Consumers Should Watch For

Credit report mistakes often appear small at first, but even one wrong entry can create major consequences. Consumers should review each report carefully for:

Accounts they never opened

Fraudulent accounts tied to identity theft

Duplicate accounts

Incorrect balances

Wrong payment history

Outdated negative information

Wrong name, address, or Social Security number

Accounts listed as late despite timely payments

Collection accounts that are inaccurate, paid, settled, or unfamiliar

These errors should be documented clearly before a dispute is submitted.

Gather Evidence Before Sending A Dispute

A strong dispute starts with strong documentation. The attached source recommends gathering account statements, creditor correspondence, identity theft reports, and proof of resolved disputes from prior investigations.

Useful evidence may include:

Billing statements

Payment confirmations

Settlement letters

Police reports or identity theft reports

Court records

Creditor letters

Prior dispute results

Screenshots or account records

Certified mail receipts

R23 Law's California Consumer Protection Attorneys often review these documents to evaluate whether a credit bureau, creditor, debt collector, or furnisher failed to properly investigate and correct inaccurate reporting.

R23 Law's Expert Legal Services For California Credit Report Error Victims

R23 Law's California Consumer Protection Attorneys handle credit reporting claims involving Experian, Equifax, TransUnion, banks, lenders, credit card companies, debt collectors, furnishers, and identity theft-related accounts.

Our firm evaluates whether the credit reporting agency or furnisher failed to conduct a reasonable investigation, continued reporting unverifiable information, ignored supporting documents, or allowed damaging errors to remain on a consumer’s credit file.

Learn more about the firm through About R23 Law, meet the attorneys through Our Team, or begin through Contact Us.

Dispute Credit Report Errors In Writing

Consumers may submit disputes online, by mail, or by phone, but written disputes create a stronger paper trail. The attached source notes that mailed disputes should include a written letter explaining the errors, relevant information, and supporting documentation, and that certified mail with return receipt provides proof the dispute was received.

A dispute letter should clearly identify:

The consumer’s name and contact information

The credit bureau receiving the dispute

The inaccurate account or item

The reason the information is wrong

The correction requested

The documents supporting the dispute

Consumers should keep a complete copy of everything sent.

Creditors And Furnishers Also Matter

Credit report disputes should not stop with the credit bureaus. The attached source recommends contacting the creditor or company that supplied the inaccurate information because furnishers may also be responsible for correcting errors under the FCRA.

For example, if a bank reports a loan as delinquent when it was paid on time, the consumer may dispute the error with both the credit bureau and the bank. If a debt collector reports an account that does not belong to the consumer, the dispute should identify why the account is inaccurate and include supporting evidence.

The 30-Day Investigation Window

After a dispute is submitted, the credit reporting agency generally has 30 days to investigate and correct errors. The attached source explains that consumers should monitor mail and email during the dispute process, and that if the dispute is resolved in the consumer’s favor, the agency must update the report and send a free copy of the corrected report.

If the dispute is denied, the credit bureau should provide an explanation. A denial does not always mean the reporting is accurate. It may mean the dispute needs stronger documentation, a renewed strategy, or legal action.

When Credit Bureaus Refuse To Correct Errors

If credit bureaus or furnishers fail to properly investigate, continue reporting false information, or ignore documentation, consumers may have legal claims. The attached source notes that legal action may be appropriate when unresolved credit report errors cost a consumer a job, credit, loans, housing, an apartment, insurance, or higher insurance premiums.

R23 Law's California Consumer Protection Attorneys pursue accountability when inaccurate credit reporting causes financial harm, emotional distress, reputational damage, or lost opportunities.

Identity Theft And Credit Report Disputes

Identity theft-related credit errors require fast action. Fraudulent accounts can spread across credit reports, trigger collection calls, and damage a consumer’s ability to obtain credit.

The attached source recommends additional protective steps when errors may be tied to identity theft, including placing a fraud alert or security freeze and reporting the identity theft to the Federal Trade Commission.

R23 Law's California Consumer Protection Attorneys represent identity theft victims dealing with false accounts, collection accounts, unauthorized inquiries, and companies that refuse to remove fraudulent reporting.

Clean Reports, Strong Rights, Real Accountability

Credit reporting companies and furnishers must take consumer disputes seriously. When they fail to correct inaccurate or unverifiable information, the consequences fall on the consumer — denied loans, higher rates, housing problems, insurance issues, and damaged credit.

R23 Law's California Consumer Protection Attorneys stand with Californians facing credit report errors, failed disputes, identity theft accounts, and unlawful reporting practices.

Contact R23 Law Today

Credit report errors can continue damaging your financial life until they are corrected. If Experian, Equifax, TransUnion, a creditor, lender, bank, or debt collector has failed to fix inaccurate reporting, R23 Law's California Consumer Protection Attorneys can review your rights and legal options.

Toll-Free — 310-598-1588