DOUBLE-BOOKED DEBT — When Student Loans Show Up Twice and Your Credit Pays the Price

Duplicate student loan balances can inflate your debt and damage your credit profile

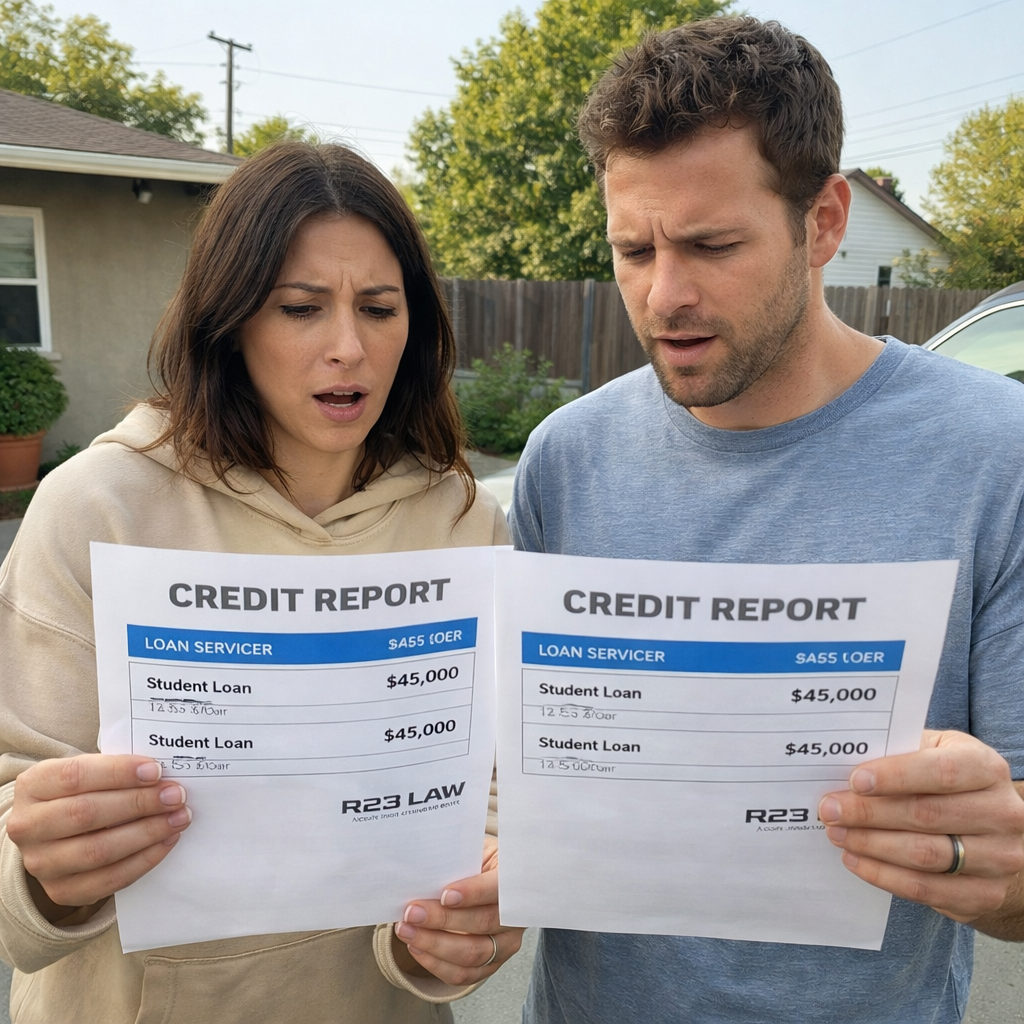

Learn common student loan credit reporting errors and FCRA dispute rights with R23 Law’s California Consumer Protection Attorneys.

Seeing one student loan on your credit report is normal. Seeing the same loan twice—with two balances that make it look like you owe double—is a different story.

The attached article flags this exact issue: duplicate balances, where the same student loan appears multiple times on a credit report, inflating total debt and creating real financial consequences. If you’re preparing for a mortgage, refinancing, a car loan, or even a rental application, that “double-booked” debt can change the outcome.

For borrowers dealing with credit reporting mix-ups, R23 Law’s California Consumer Protection Attorneys approach these problems through a consumer protection lens: accuracy, accountability, and damages when reporting errors cause harm.

What Duplicate Student Loan Balances Look Like

Duplicate balances typically show up as one loan listed multiple times—often under different names or tradelines—so your report suggests a higher total debt than you actually owe. The attached material explains this often happens after:

Loan servicer changes (your loan transfers and appears again under the new servicer)

Reporting errors (a bureau or furnisher updates incorrectly and creates duplicate entries)

Consolidation issues (the original loans and the consolidation loan both show as active)

Even when every monthly payment is on track, duplication can make your profile look riskier than reality.

Why This Error Hits Hard

A duplicate balance isn’t just annoying—it can be expensive. Inflated student loan debt can:

raise your debt-to-income ratio

reduce borrowing power for a mortgage or auto loan

trigger higher interest rates or stricter terms

create delays while lenders request clarifications and re-check credit

Bottom line: your credit report is often treated as a scoreboard. Duplicate balances rig the score.

Three Other Student Loan Credit Reporting Errors That Keep Reappearing

In addition to duplicate balances, the attached piece highlights three repeat offenders in student loan credit reporting:

Incorrect payment status

Loans may be reported as delinquent or in default even when payments were made on time.

Misreported loan amounts

The balance or original loan amount may be overstated, making it appear you owe more than you do.

Closed loans still showing as open

Paid-off loans or loans closed through consolidation may still appear active, artificially inflating your debt load.

Each of these errors can drag down your credit standing and create knock-on effects across financing decisions.

FCRA Rights That Matter When Student Loans Are Reported Wrong

The article summarizes key protections under the Fair Credit Reporting Act (FCRA) for credit report inaccuracies tied to student loans:

Right to dispute errors: You can dispute inaccurate or incomplete information; both the credit reporting agency and the furnisher (often the servicer) must investigate.

Right to accurate information: Credit files must be maintained accurately and updated when errors are identified.

Right to pursue legal action: If disputes don’t resolve the problem—or the error causes measurable harm—you may have claims for damages.

These rights are especially important when the error is persistent, repeats after “corrections,” or blocks you from credit you would otherwise qualify for.

A Clean Dispute Blueprint for Duplicate Balances

The attached piece lays out a straightforward process borrowers can use to build a record and push for correction:

Review your credit reports from Experian, Equifax, and TransUnion (the article notes obtaining free reports through AnnualCreditReport.com).

Identify and document the issue (duplicate tradelines, incorrect status, wrong balance, or closed loans listed as open).

Submit a dispute with supporting documentation, such as loan statements, payment histories, or consolidation paperwork.

Follow up and monitor to confirm the correction actually sticks.

If a duplicate balance disappears and then reappears, that’s not “normal churn.” It can signal a deeper reporting failure worth a closer legal review.

Where R23 Law’s California Consumer Protection Attorneys Enter the Picture

When student loan credit reporting errors persist after disputes—or when a duplicate balance causes a denial, higher interest rate, or lost opportunity—R23 Law’s California Consumer Protection Attorneys evaluate whether the credit bureaus and furnishers followed their legal obligations and whether the consumer suffered recoverable damages.

Disclaimer: This content is for informational purposes only and does not constitute legal advice.