THE MORTGAGE DENIAL PLOT TWIST — Credit Report Errors Crashing the Closing Table

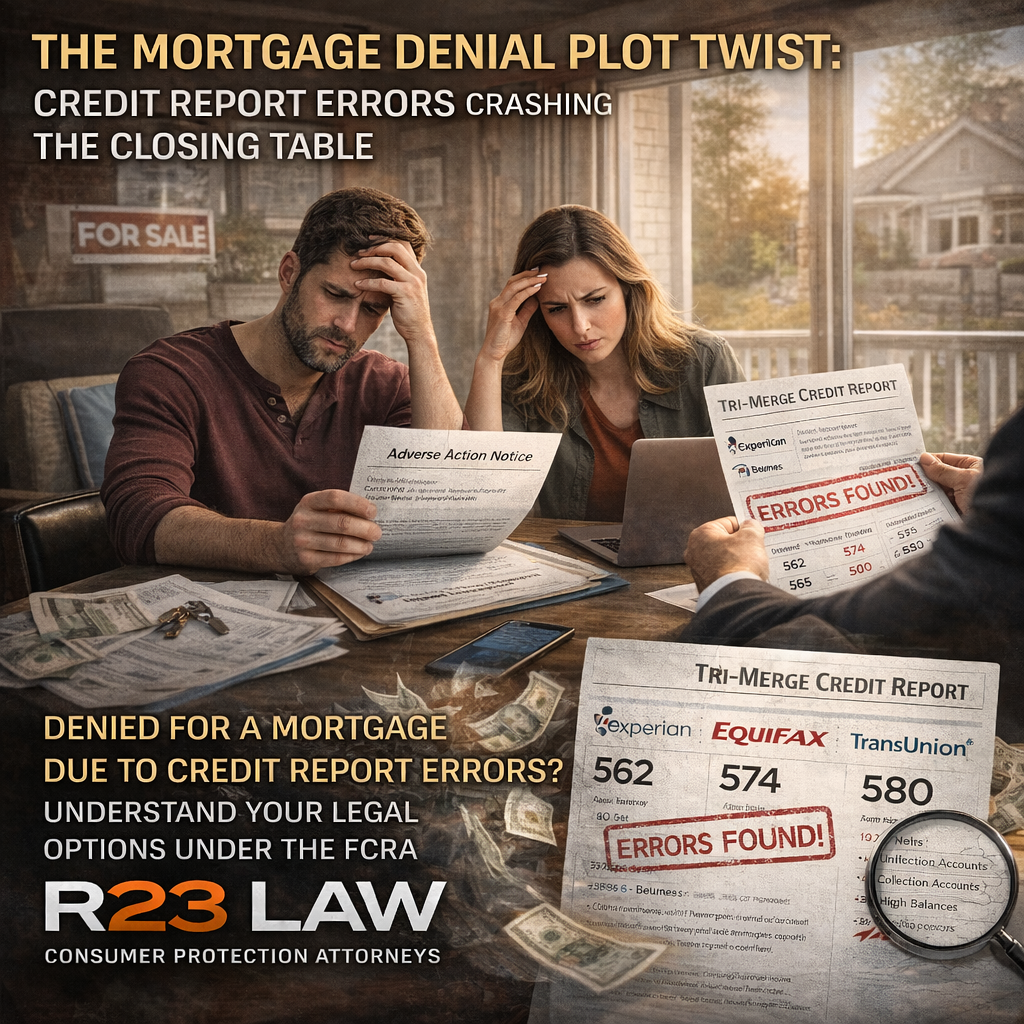

Denied for a mortgage or loan due to credit report errors?

Learn the fast, documented steps under the FCRA—what to pull, what to dispute, and what to preserve for damages.

Buying a home is supposed to feel like momentum—preapproval, paperwork, keys. Instead, many consumers hit a wall at the worst possible time: a mortgage or loan denial based on credit report errors. And when timing matters (rate locks, earnest money deadlines, moving plans), a “credit file problem” becomes a real-life financial emergency.

The frustrating part: the denial may have nothing to do with your actual credit behavior. It can stem from false accounts, mixed files, outdated data, or identity theft entries that never should have been on your reports in the first place.

Below is a clear, documentation-first playbook—built around the same steps lenders and credit bureaus rely on—plus where federal consumer protections can create legal exposure when inaccurate reporting causes measurable damage.

Start With the Denial Letter and the Credit Report Source

When a lender denies credit, you’re typically entitled to an explanation of the decision and which consumer reporting agency (CRA) provided the report. If your lender used credit report information to make an adverse decision, the Fair Credit Reporting Act (FCRA) also requires an adverse action notice with key disclosures, including the CRA’s contact info and your right to obtain a free copy of your report and dispute inaccuracies.

Action item: locate the denial/adverse action notice and identify:

which CRA or report provider was used (Experian, Equifax, TransUnion, or a reseller),

whether a credit score was referenced,

and any stated reason codes (e.g., “delinquency,” “high utilization,” “collection account”).

Pull the Exact Version of the Report the Lender Saw

Many mortgage decisions rely on a tri-merge report (data combined from all three bureaus) or a “residential mortgage report” from a reseller. The article specifically notes resellers frequently used in mortgage lending, including CoreLogia, Credit Plus, and LexisNexis.

Why this matters: your “consumer-facing” credit monitoring snapshot can look different from akage. You want the same data set that triggered the denial.

Audit for the Big Three Credit Report Error Categories

Once you have the report(s), review line-by-line. The most denial-driving errors tend to fall into three buckets:

1) Accounts that aren’t yours

unfamiliar credit cards, loans, or auto accounts

authorized user accounts you never agreed to

collections tied to unknown creditors

2) Personal information mismatches

wrong addresses, employers, or variations that don’t beltors of a “mixed file” (someone else’s data stitched into yours)

3) Outdated or incorrect reporting

“late” payments you can prove were on time

balances ements

accounts that should be closed, deleted, or updated

Dispute the Errors With Documentation You Can Prove

If you find mistakes, the next step esponsible CRA. The article notes you can dispute online, but a detailed letter (often sent via certified mail) creates a stronger record of what you submitted.

Under the FCRA, when you dispute information, the CRA generally must reinvestigate and complete t30 days**, with a possible limited extension if you provide additional relevant information during the investigation window.

Build a dispute package that reads like evidence:

a copy of the report with the wrong items highlighted

a numbered list of what’s wrong and the correction requested

supporting documents (ID theft report, account statements, payoff letters, identity documents, court records—depending on the error)

a copy of your ID and proof of address (so the dispute isn’t rejected as “incomplete”)

Track What the Credit Bureau Does Next

After reinvestigation, the CRA will send results. The article notes outcomes can include correction, modification, or no change—and if corrections occur, the CRA may also notify the lender.

Practical tip: keep a timeline (date sent, method, tracking, response date, outcome). In consumer protection matters, the paper trail often determines leverage.

A credit report error can trigger:

higher interest rates

loss of a rate lock

denial of a mortgage, auto loan, or refinance

additional deposits required for utilities or housing

lost housing opportunities (and real dollars tied to it)

When inaccurate credit reporting causes measurable harm—and the dispute process still produces a “verified” result—this can move from a correction problem to a compliance problem.

That’s where R23 Law's California Consumer Protection Attorneys step in: evaluating the dispute record, the investigation conduct, and whether the facts support claims tied to wrongful credit reporting and resulting damages.

Key Takeaway

A loan denial based on credit report errors calls for speed and documentation. Get the denial details, pull the same reports the lender relied on (including tri-merge/reseller reports when applicable), identify the exact errors, and dispute with a record that holds up.

If inaccurate reporting continues after disputes—or the denial created significant financial fallout—R23 Law's California Consumer Protection Attorneys can assess the legal options available under federal consumer protection law.

Disclaimer: This article is for informational purposes only and does not constitute legal advice. Reading this article does not create an attorney-client relationship.